Working as a locum tenens physician offers flexibility, higher earning potential, and control over your schedule; however, it also requires you to manage your own taxes. Unlike W-2 employees, locum tenens physicians are typically paid as independent contractors, meaning there is no automatic tax withholding and more responsibility on your end.

The good news: With proper planning, strong recordkeeping, and an understanding of how 1099 taxes work, you can reduce your tax bill, avoid penalties, and stay compliant across multiple states.

Here, we walk through how locum tenens taxes work, which deductions matter most, and what to do after you accept an assignment.

1099 vs. W-2 taxes: Why locum tenens taxes work differently

Understanding the differences between 1099 and W-2 classifications for locum tenens work is a crucial starting point.

Most locum tenens physicians are classified as independent contractors and receive a Form 1099-NEC instead of a W-2. A 1099 only reports income; there are no deductions for federal income tax, Social Security, or Medicare.

This classification creates two significant differences:

- You are responsible for paying your own taxes, including quarterly estimated payments.

- You can deduct “ordinary and necessary” business expenses related to earning your income. The Internal Revenue Service (IRS) defines these expenses as “An ordinary expense is common and accepted in your industry. A necessary expense is helpful and appropriate for your trade or business. An expense does not have to be indispensable to be considered necessary.”

If you work both W-2 and 1099 jobs, deductions generally apply only to your 1099 income. This distinction is crucial when allocating expenses for continuing medical education (CME), licensing, and travel.

Self-employment tax and quarterly estimated payments

As a 1099 physician, you pay self-employment (SE) tax, which covers Social Security and Medicare. The current SE tax rate is 15.3% on net earnings, in addition to federal and state income taxes.

Because nothing is withheld from your paychecks, the IRS requires you to make quarterly estimated tax payments using Form 1040-ES. These are generally due April 15, June 15, September 15, and January 15 (note the extension for Q4 to accommodate the holidays).

Failing to pay enough throughout the year can trigger underpayment penalties, even if you pay everything by April.

A common rule of thumb is to set aside 25-35% of 1099 income, but the correct amount depends on the income level, deductions, and state taxes. Guessing is how locum tenens physicians with 1009 work get surprised in April.

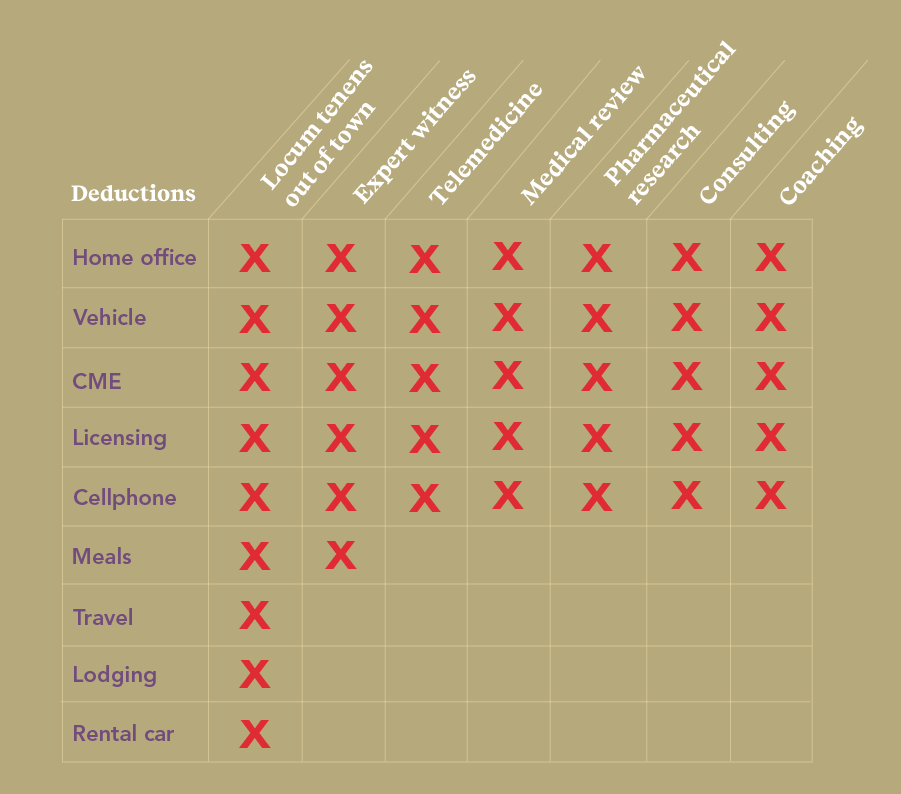

Common tax deductions for locum tenens physicians

Here’s an example of some everyday expenses 1099 physicians deduct:

Your marginal tax rate is the tax rate on the next dollar of income. It would be best if you used your marginal rate when quantifying the benefit of a deduction because that’s the amount by which your tax will change.

This differs from your effective tax rate, which is calculated by dividing your total tax by your total income. If we used your effective tax rate to measure the benefit of a deduction, we would understate the tax savings.

Let’s dive deeper into the nuances of each of these general categories.

1. Business travel

If you drive to assignments, you can deduct mileage using the IRS standard mileage rate or actual vehicle expenses.

The standard mileage rates for 2026 are:

- Self-employed and business: 70 cents/mile

- Charities: 14 cents/mile

- Medical: 21 cents/mile

- Moving (military only): 21 cents/mile

Flights, rental cars, lodging, and baggage fees may also be deductible when not reimbursed.

In some cases, a 100% deduction of the car’s cost, fuel (or charging for electric cars), and even car insurance premiums may be possible.

2. Meals … for free?

You can deduct the cost of meals while traveling for work as a locum tenens doctor. This deduction is especially beneficial if you are working in a major city with a high cost of living. You may deduct meals either at actual cost or at a per diem rate, depending on your situation.

Dr. Nii Darko, trauma/critical care surgeon who works locum tenens, shares:

“The calories are low and so are the taxes!”

3. Continuing Medical Education (CME) and other licensing fees

CME courses, conference travel, licensing fees, Drug Enforcement Administration (DEA) registration, board certification, and professional dues are generally deductible if they are directly related to your locums work. These deductions can really add up, especially if you are attending multiple conferences or courses throughout the year.

Remember, as long as the expenses are business-related, they may qualify for a tax deduction. No need to confine yourself to online credits. Go to that conference in a tropical location if you’d like!

4. Scrubs, gadgets, and equipment are all write-offs

One of the many perks of being a locum tenens is deducting the cost of your phone, gadgets, clothes, and medical equipment. Using your phone, tablet, and/or computer in any work-related fashion can justify a tax deduction.

Do you need a new stethoscope, scrubs, scrub shoes, or a white coat? Well, since you’ll be using these during your locums assignment, they are tax-deductible.

5. Free or reduced lodging

Wherever your assignment takes you, you can deduct your lodging. Apart from seeing the world while doing what you love, you also get to visit and live in some pretty amazing places for free.

Most locum tenens agencies will cover the cost of your lodging, so while not a real tax deduction, it certainly is a money saver. If by some chance you have a hotel expense related to acquiring or working during an assignment, then a tax deduction is very likely.

6. Home office deductions

If you are working as a locum tenens doctor, there’s a good chance you are doing at least some administrative work related to business from home. Whether that involves taking phone calls, answering emails, participating in conference calls, or conducting telemedicine, designating a home office is a great way to claim a tax deduction.

If you use part of your home regularly and exclusively for administrative locums work, you may deduct a portion of your rent, mortgage interest, utilities, and internet expenses.

You can deduct a portion of your rent, mortgage interest, utilities (including internet), and other home office expenses. “I even have my business write a check for rent to make it more official and easier to document,” says Dr. Darko.

7. Health insurance

“Barring any special circumstances, any locum doctor should be able to get health insurance and get it deducted as a business expense,” advises Dr. Darko.

Many doctors worry about their ability to obtain health insurance as independent contractors. Well, health insurance is available in the marketplace.

8. Malpractice insurance

If you pay for malpractice coverage yourself, premiums are deductible. Coverage provided by agencies is not.

Dollars and cents: Learn how locums pay and salary work

Deductions by type of 1099 work

How multi-state taxes and California withholding rules apply to locums

Locum physicians frequently earn income in multiple states. In general:

- You pay state income tax where the work is performed

- Your home state may tax the income as well, but usually offers a credit for taxes paid to other states

California deserves special attention. California requires nonresident withholding on California-source income unless you submit Form 590, certifying exemption. Without it, agencies may automatically withhold state tax.

Keep meticulous records of:

- Income by state

- Days worked per assignment

- State-specific expenses

- Should you form an LLC or an S-Corp?

California is aggressive in enforcement, and sloppy records are an open invitation for an audit.

Many locum physicians operate as sole proprietors by default; however, understanding when and why to consider forming an LLC or S-Corp can be a smart financial move.

In short, forming an LLC or electing S-Corp status can make sense, but only when income justifies the added complexity. Potential benefits include liability separation (note that this differs from malpractice protection), additional retirement planning options, and, with an S-Corp, possible self-employment tax savings. Most locum physicians opt to use a professional tax advisor to handle all their business details.

If you don’t understand why you are forming an entity, you are probably not ready to form one.

Experienced locum and emergency medicine physician Dr. Rip Patel states:

“If it makes sense, you can be taxed as an S-Corp rather than as a disregarded entity. This requires some additional administrative work to ensure compliance with the IRS, but it could potentially save you money on your self-employment taxes. However, creating that extra layer of liability protection is an important aspect, in my opinion.”

How to stay audit-ready

Audit risk isn’t driven by taking legitimate deductions; it’s driven by poor documentation.

According to Alexis Gallati of Cerebral Tax Advisors, the most common mistake independent contractors make is not keeping track of their expenses or their income. That’s why it’s essential to keep receipts for everything from the time you leave your home for an assignment to the time you come back—and possibly in between.

Another must? Keep the original receipts or copies; the IRS will not accept bank or credit card statements as proof. “It can be as easy as setting up a Google Drive or a cloud-based system; you do not have to have the physical receipts, just a picture or digital image will work,” she says.

In short, best practices for tracking your business expenses as a locum tenens physician include:

- Digital copies of receipts (bank statements are not enough)

- Separate checking account for 1099 income and expenses

- Mileage logs and travel documentation

- Assignment contracts showing length and location

Keep records for at least seven years. If you cannot substantiate a deduction, assume it will not survive scrutiny.

Pensions, SEPs, and savings for 1099 physicians

As an independent contractor, you will be responsible for creating your nest egg for retirement. Emergency medicine physician Dr. Jim Mock—with the help of his accountant—has a solid plan in place to prepare for his future retirement, explaining that he has a two-part pension plan:

Gallati recommends the Solo 401(k) over the SEP IRA because, with a Solo 401(k), you can contribute the maximum employee amount of $22,500 (or $30,000 if you’re 50 or older). In contrast, with an SEP IRA, you’re limited to 25% of your compensation into a retirement account. Both have maximum contributions of $66,000 (as of 2024).

When setting up retirement accounts, Gallati advises establishing an S Corp or PLLC, which will enable you to make the most of your retirement contributions.

“There’s a new QBI deduction, and most independent contractors are making over that $315,000 (or up to $415,000 if married filing jointly) max income to take advantage of that deduction. A retirement deduction can help lower your income,” she says.

What to do after accepting a locums assignment

Once you accept an assignment, the tax clock starts immediately. What you do in the first few weeks determines whether tax season is routine or painful.

- Submit a W-9 to your agency. This establishes how you’ll be paid and how you’ll be reported to the IRS. Errors here cascade into incorrect 1099s, delayed payments, and avoidable cleanup later.

- Confirm tax classification (1099 versus W-2). Never assume. Some assignments are W-2, others are 1099, and the tax rules differ materially. Misclassifying income leads to incorrect deductions and penalties.

- Track income and expenses from day one, including diligent receipt tracking. Reconstructing expenses months later is how deductions disappear. Track everything in real time or accept that you will overpay.

- Set aside money for quarterly taxes. Separate the money as you earn it so it’s unavailable for spending.

- Log travel days and locations. Working across multiple states creates tax obligations across multiple states. If you don’t track where and when you worked, you are guessing, and the IRS does not accept guesses.

- Review state-specific tax rules. Each state plays by its own rules, and some (like California) enforce them aggressively.

- Consult a tax professional before year-end. December planning can save real money.

Hear from the experts: How to maximize your tax benefits as a locum

The following webinar features experienced locum physician Dr. Patel and tax experts Alexis Gallati and Skylar Campbell, who share strategies for maximizing tax benefits as a locum tenens physician. Watch the full webinar below.

Managing taxes as a locum doesn’t have to be stressful

With good record keeping, planning, and the proper guidance, you can maximize deductions and minimize surprises while staying compliant with IRS and state rules.