Nearly 7% of the U.S. workforce is made up of independent contractors, which includes locum tenens physicians. Instead of automatic deductions for Social Security, federal and state income taxes, FICA, and Medicare, taxes work differently for independent contractors. This guide will help you understand how to plan for, prepare, and manage locum tenens taxes.

Employee vs. independent contractor

Locum tenens physicians, by definition, are independent contractors. They do not receive benefits or get automatic deductions from the facility in which they work or from the locums agency they’re working for. Instead of receiving a W-2 with automatic deductions at the end of the year, they will receive a 1099-MISC from each business client, which simply reports income earned. There are no automatic deductions on a 1099-MISC. This is where a tax professional can help.

One physician’s take: The financial side of locums: What’s your strategy? (Weatherby Healthcare)

The top 5 locum tenens tax considerations

Although the taxes are the least fun part of working locum tenens, don’t let this be a deterrent. Once you have a good system in place, it’s not any harder to take care of your taxes than it would be for any small business owner. Of course, finding a reputable tax professional with experience in locum tenens physicians’ finances is worth every penny, because they will help you develop a good system.

According to Alexis Gallati of Cerebral Tax Advisors, here are the top 5 things to remember:

- You must give your agency your Form W-9 before beginning your first assignment.

- You have to pay income tax on income you earn as you earn. For W-2 employees, this is done on their behalf each paycheck. As a 1099 employee, you must make quarterly estimated tax payments.

- Quarterly estimated tax payments must be made on time to avoid penalties. They are generally due on the 15th of April, June, September, and January.

- The amount of estimated tax you need to pay depends mostly on your prior year’s taxable income and credits. You may need to pay as little as 90% of last year’s tax liability, but as high as 100%.

- Failure to do the above will result in an estimated tax penalty, which is 0.5% of the amount unpaid for each month the tax isn’t paid.

Tracking and reporting expenses as a locum physician

Gallati says the most common mistake independent contractors make is not keeping track of their expenses or their income. That’s why it’s important to keep receipts for everything from the time you leave your home for an assignment to the time you come back — and possibly in between.

Another must? Keep the actual receipts or a copy; the IRS won’t accept bank or credit card statements. “It can be as easy as setting up a Google Drive or a cloud-based system; you don’t have to have the physical receipts, just a picture or digital image will work,” she says.

“Additionally, be aware of those things your agency is covering, like travel, meals, and incidentals, and make sure you’re not writing off expenses that are being reimbursed by the agency.”

Whether you have a per diem expense allowance is dependent primarily upon:

- The length of assignment. If your assignment is longer than one year, this allowance doesn’t apply. But if your assignment lasts one year or less, your employment is treated as temporary. “The term of assignment should be for a definite period of time and documented,” Gallati says. “If the assignment is reasonably expected to last for one year or less, but it’s later discovered that employment is expected to exceed one year, the employment will be treated as temporary until the date the expectation changes.”

- The distance from your permanent residence. It must be 50 miles or greater, generally with overnight stays.

Be sure to discuss with your tax professional whether actual expenses or a per diem applies. You’ll want to be sure to get credit for all of the work-related expenses you are eligible for.

What’s the difference? How locums jobs and perm jobs compare

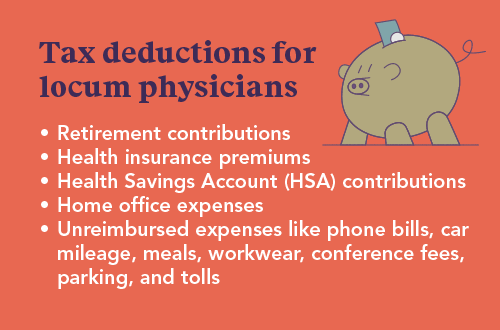

Locum tenens physician tax deductions

Another nice aspect of being an independent contractor is that it is far easier to take business-related tax deductions. Anything you spend on your business — including scrubs, white coats, shoes, computers, phones, CME materials, licensing fees, subscriptions, mileage, and more — can be placed directly on Schedule C (assuming sole proprietorship, but the process is similar for partnerships and corporations) as a business expense. These expenses are deducted from the business income before any taxes, including payroll taxes, and you are paid on that income. It is super easy.

LEARN MORE: 7 tax benefits of being an independent contractor

How to choose a business entity

There are many options for setting up a business entity when beginning work as an independent contractor. Depending on your situation, it may make more sense just to file as self-employed without creating a formal business entity.

If your situation merits the creation of a business or tax entity, two of the most popular for locums physicians are LLCs and S corporations. There are two crucial differences between an LLC and an S Corp: an LLC is a business structure legally separating the business and the individual, and an S Corp is an election that indicates how the business (physician) is taxed. The benefit of both is you can protect your personal assets from creditors of your business. However, this does not include protection from a malpractice lawsuit. If you’re working with an accredited locum tenens agency, though, they’ll typically offer comprehensive malpractice coverage.

Emergency medicine physician Dr. Jim Mock chose to create an S corp. He’s found for him, there are tax advantages. He pays himself a monthly base salary, and if he exceeds his base salary he does a shareholder distribution that’s taxed a little differently than his base salary.

“Of course, I coordinate all of that with my accountant to be within federal regulations and tax laws,” he says.

Pensions, SEPs, and savings for 1099 physicians

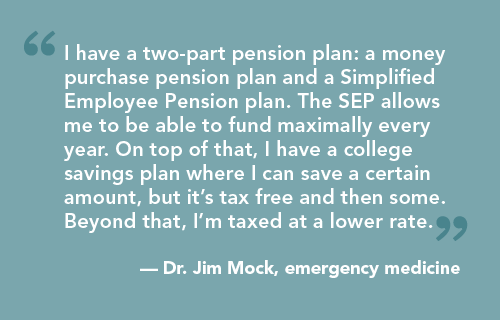

As an independent contractor, you will be responsible for creating your nest egg for retirement. Dr. Mock — with the help of his accountant — has a solid plan in place to prepare for his future retirement.

“I have a two-part pension plan: a money purchase pension plan and a Simplified Employee Pension (SEP) plan,” he says. “The SEP allows me to be able to fund maximally every year, to be prepared. On top of that, I have a college savings plan where I can save a certain amount but it’s tax-free and then some. Beyond that, I’m taxed at a lower rate.”

Gallati recommends the Solo 401(k) over the SEP IRA because with a Solo 401(k) you can put in the maximum employee amount of $22,500 (or $30,000 if you 50 or older), whereas with an SEP IRA, you’re limited to 25% of your compensation into a retirement account. Both have maximum contributions of $66,000 (as of 2024).

When it comes to looking at retirement accounts that you want to set up, Gallati says you may want to consider setting up an S Corp or PLLC that will allow you to maximize your ability to make retirement contributions.

“There’s a new 199A or QBI deduction (one and the same), and most independent contractors are making over that $315,000 (or up to $415,000 if married filing jointly) max income to take advantage of that deduction. A retirement deduction can help lower your income,” she says.

Have a tax plan before you start working locums

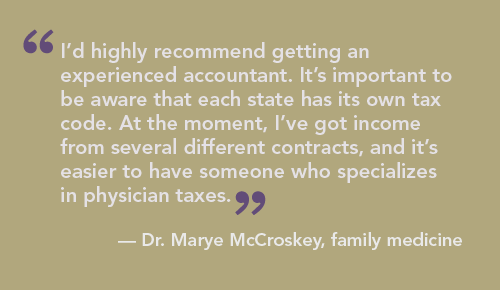

After nearly 30 years in private practice, family medicine physician Dr. Marye McCroskey was ready to try something different. She decided to try her hand at locum tenens, but she and her husband didn’t jump into it without some pre-planning.

“I’d highly recommend getting an experienced accountant,” she says. “It’s important to be aware that each state has its own tax code. At the moment, I’ve got income from several different contracts, and it’s easier to have someone who specializes in physician taxes.”

The tax benefits can outweigh the burden for locum physicians

Locum tenens work brings many physicians the work/life balance they’re craving. Although this lifestyle can mean a little more administrative work, it’s worth the increased freedom, schedule flexibility, and opportunity for career growth. With a little help from a qualified tax professional, locum tenens taxes can be an easily managed part of a fulfilling career as a locum physician.